Kimi’s Sudden IPO Plans: A Rapid Shift in Strategy

On December 31, 2025, Yang Zhilin, the founder of Kimi’s parent company Moonlight, stated in an all-staff letter: “We are not in a hurry to go public in the short term, nor is going public our goal.” At that time, the company had just completed a $500 million Series C funding round, with a valuation of $4.3 billion and over 10 billion RMB in cash. Everything seemed calm.

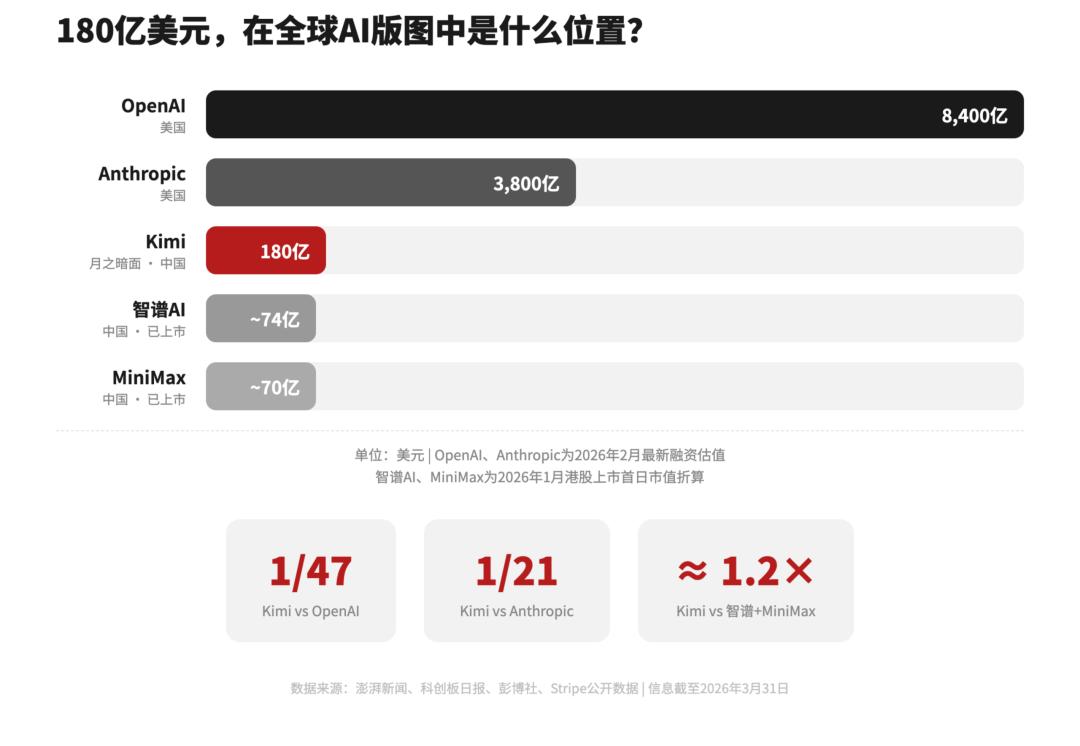

However, less than three months later, Bloomberg reported that Moonlight was evaluating the possibility of an IPO in Hong Kong and was in preliminary discussions with China International Capital Corporation and Goldman Sachs. By this time, Kimi’s valuation had soared to $18 billion, quadrupling in just three months.

What led to this shift from “not in a hurry” to seeking an IPO? Analyzing Kimi’s rapid acceleration reveals a microcosm of the entire AI industry transitioning from a focus on technical storytelling to tangible business results. This is not just a valuation myth for one company.

If we rewind to a year ago, Kimi’s script was entirely different.

1. Monthly Active Users Plummet by 50%, Entering the List of “Most Declining AI Companies”

In early 2025, DeepSeek emerged, shaking the entire industry with its open-source model and ultra-low-cost strategy. Kimi faced a direct and severe impact. At that time, the company was criticized for its “money-burning customer acquisition” strategy, leading to a significant reduction in product launch budgets under internal and external pressure.

According to QuestMobile data, Kimi App’s monthly active users plummeted from 21.65 million in Q1 2025 to 9.07 million in Q4. By the end of 2025, some tech media even labeled Kimi as one of the “most declining AI companies” based on the standard of monthly active users being less than 5%.

However, beneath the surface, Moonlight made a crucial strategic pivot. In Yang Zhilin’s year-end letter, he mentioned that in 2026, they would focus on “agents in product and commercialization, not targeting absolute user numbers, but continuously pursuing the upper limits of intelligence to create greater productivity value and achieve exponential revenue growth.”

2. Betting on the AI Agent Track, Four Technical Collisions with DeepSeek

From stopping the money-burning advertising to fully betting on Agents, Moonlight concentrated its chips on one bet: Agents are the true commercial application scenarios for large models.

There are overseas precedents that validate this path. Cursor achieved an annual recurring revenue (ARR) of $2 billion in 20 months, while Claude Code reached $1 billion in ARR just nine months after its launch, both relying on the same logic: selling productivity, not conversations. Moonlight’s bet is the Chinese version of this logic.

Throughout 2025, Yang Zhilin and DeepSeek founder Liang Wenfeng had four precise “collisions” in technology: reinforcement learning inference in January, sparse attention architecture in February, mathematical self-verification in April, and visual understanding on January 27, 2026. Each collision represented a fiercely contested frontier in the industry. The difference is that DeepSeek focused on foundational technological breakthroughs, while Kimi took an additional step—packaging its technological capabilities into usable Agent products.

In January, Kimi K2.5 was officially released and open-sourced, marking the first major move after Moonlight’s strategic pivot. This model is based on a trillion-parameter mixture of experts (MoE) architecture, utilizing 15 trillion visual and text mixed tokens for native multimodal training, achieving significant advancements in agent intelligence, code generation, and visual understanding. A few weeks later, Kimi’s website also launched Kimi Claw, bringing the entry point for using Agents directly into the browser.

3. Paid Orders Surge by 82 Times, ARR Breaks $100 Million in 30 Days

Following the launch of K2.5 and Kimi Claw, Kimi reversed its downward trend.

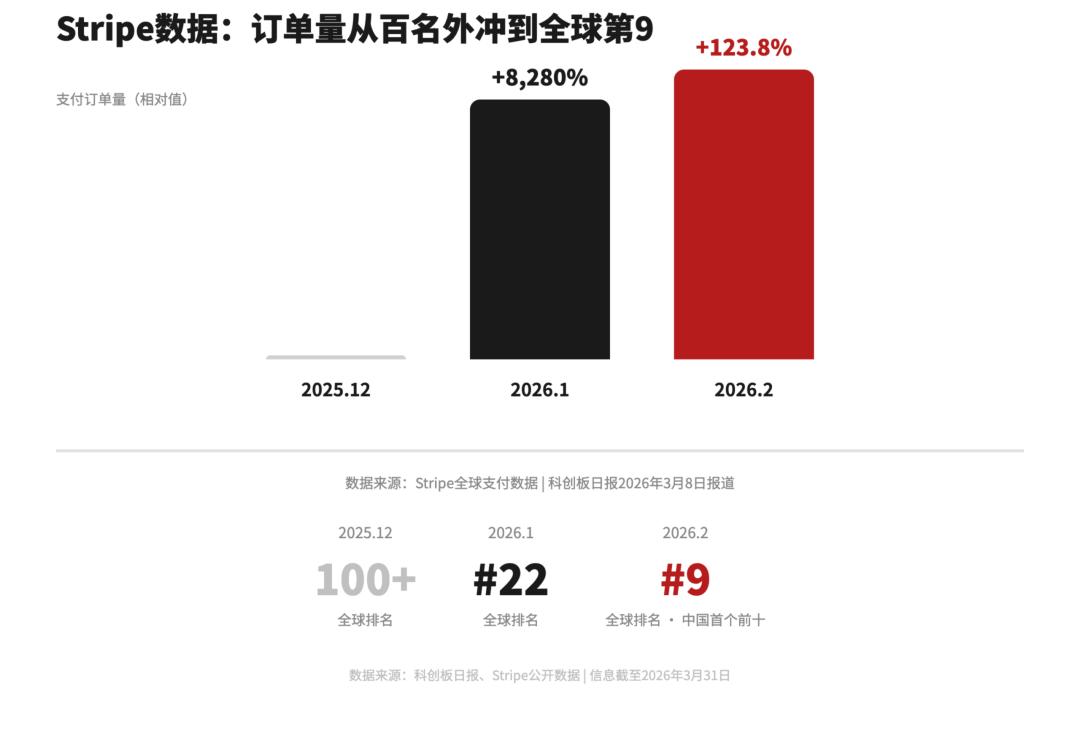

According to global payment giant Stripe, the payment order volume from Kimi’s individual subscription users surged by 8280% (82.8 times) month-on-month in January 2026, with a further increase of 123.8% in February. Kimi’s ranking on Stripe’s global leaderboard skyrocketed from outside the top 100 to 9th place, becoming the first Chinese AGI product to break into the top ten.

As reported by Interface News on March 30, just one month after the release of K2.5, Moonlight’s ARR (annual recurring revenue) exceeded $100 million, making it the first company among the “AI Six Tigers” (Zhipu AI, MiniMax, Baichuan Intelligence, Moonlight, Jietiao Xingchen, and Lingyi Wantu) to reach this milestone.

Multiple media outlets reported that within 20 days of K2.5’s launch, Kimi’s cumulative revenue had already surpassed its total revenue for the entire year of 2025. This is the hard logic behind the fourfold increase in valuation over three months—capital only pays a premium for turning points. Kimi’s turning point was not about larger model parameters or higher benchmark scores, but about getting users to willingly pay.

In the industry, Kimi’s capabilities also received an unexpected endorsement. On March 19, Cursor released its new model Composer 2, which was discovered by developers to be fundamentally built on Kimi K2.5—this AI programming unicorn valued at $50 billion chose to drive its core product with a Chinese model.

In the same month, Yang Zhilin was the only invited Chinese independent large model founder to speak at NVIDIA’s GTC conference.

4. $2.9 Trillion Unicorns Queuing for IPO, Hong Kong Stock Window Won’t Wait

The attitude flip in 86 days may not necessarily be a slap in the face, but rather the market window won’t wait. 2026 has been dubbed by Wall Street as the “super IPO year”—nearly $2.9 trillion worth of private enterprises are poised to go public, with AI being the absolute main character.

CoreWeave has already gone public in the US, raising $1.5 billion; Anthropic’s valuation has soared to $380 billion, planning to raise over $60 billion in a super IPO; OpenAI is advancing its IPO plan with a valuation of $830 billion. Global AI companies are collectively sprinting towards the capital market.

At the same time, Zhipu and MiniMax have already gone public on the Hong Kong Stock Exchange in January 2026, with their stock prices continuing to rise post-IPO, stabilizing their market values at around $40 billion, proving that the Hong Kong Stock Exchange’s Chapter 18C (special technology company listing mechanism) is a viable channel for unprofitable AI companies. However, the window for the Hong Kong Stock Exchange may not remain open forever.

Although Moonlight is currently only in the “initial evaluation of IPO possibilities” stage, the logic of the capital market is not hard to understand.

The primary market valuation has reached $18 billion; if the Hong Kong stock market can provide a higher secondary market pricing, early investors can profitably exit, and the company can raise new funds to expand its advantages; conversely, if market sentiment cools and leads to a valuation inversion, $18 billion could become an awkward anchor price.

5. $18 Billion Valuation Anchored, AI Money Chasing Results

Therefore, regardless of whether an IPO ultimately occurs, being prepared in advance at a high valuation and with an open window is a rational choice.

Kimi’s story may just be beginning. The $18 billion valuation is a recognition from the capital market of its commercial achievements over the past few months and an expectation of whether it can become an AI productivity platform in the future.

Notably, after the release of K2.5, Kimi’s overseas revenue has surpassed domestic revenue, with overseas API revenue growing fourfold and the monthly growth rate of global paid users exceeding 170%.

The momentum of the entire Chinese AI industry is also synchronously exploding. The “lobster craze” sweeping the internet in early 2026—represented by the open-source AI intelligent agent framework OpenClaw—has pushed Agents from the developer circle to the general public. Companies like Tencent, ByteDance, Alibaba, MiniMax, and Zhipu have all launched lobster products, leading to a surge in token usage.

According to OpenRouter data, as of March 15, the weekly token usage of Chinese AI large models reached 4.69 trillion tokens, surpassing the US for two consecutive weeks, with the top three globally being all Chinese models.

The capital market’s response has been even more direct—MiniMax’s stock price has cumulatively risen by 644% from its issue price, with its market value once exceeding 380 billion HKD; Zhipu’s market value has also surpassed 300 billion HKD. The lobster craze has proven one thing: when AI can truly do work for people, users will flock to it, and the commercialization flywheel of large models may start to turn.

Kimi’s miraculous turnaround in 86 days is just one facet of this flywheel. Large models are expensive, and if users do not pay, relying on API price wars will not cover costs—this has been the collective anxiety of the Chinese AI industry over the past two years.

Kimi’s soaring valuation and the nationwide explosion of the lobster craze provide the same answer: when AI transitions from a chat tool to a productivity tool, the money will come. Agents may not be the only answer, but they are a validated one.

Comments

Discussion is powered by Giscus (GitHub Discussions). Add

repo,repoID,category, andcategoryIDunder[params.comments.giscus]inhugo.tomlusing the values from the Giscus setup tool.